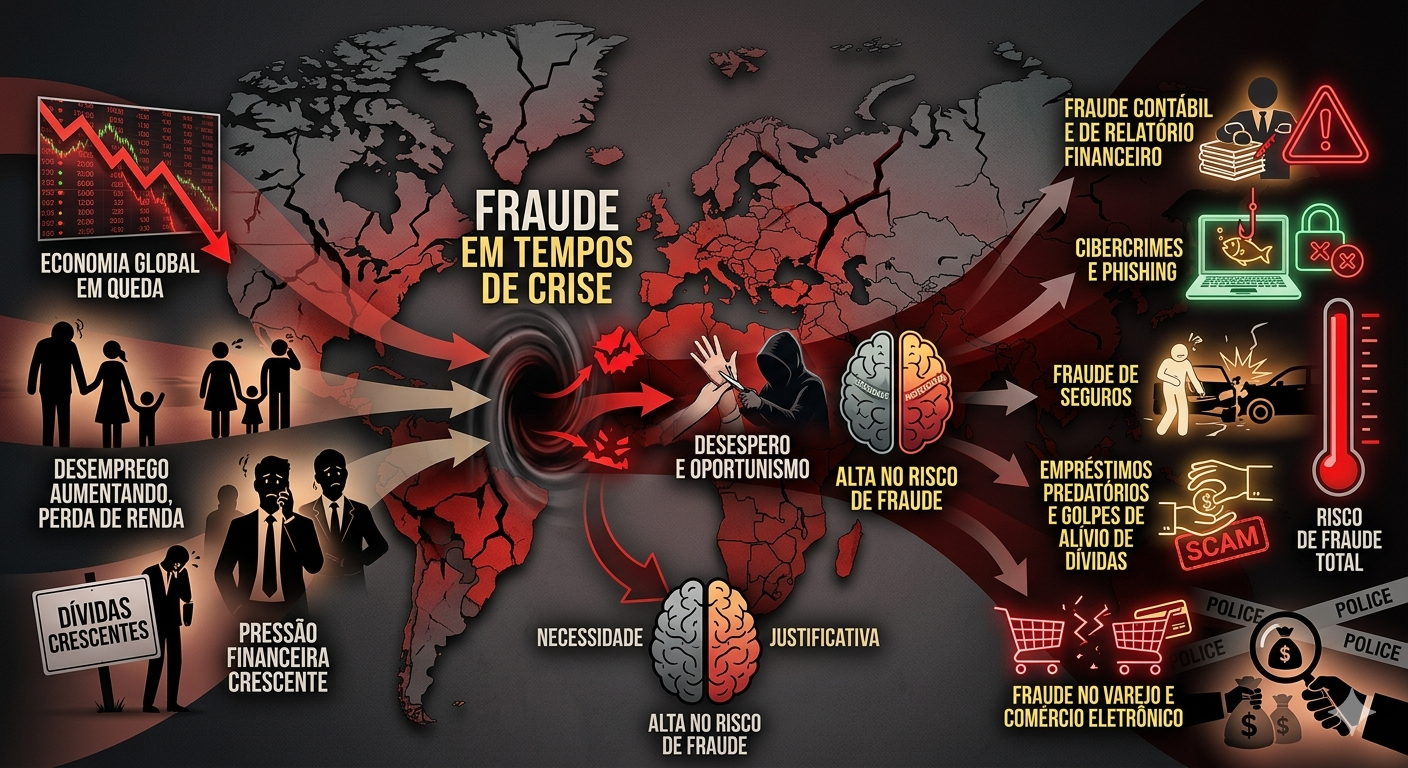

Economic stability is often viewed as the bedrock of a functioning society, providing the predictability necessary for businesses to thrive and individuals to plan for the future. However, history has shown that economic cycles are inevitable, and during periods of downturn—whether triggered by a pandemic, a banking collapse, or geopolitical instability—the landscape of financial crime shifts dramatically. One of the most significant, yet often overlooked, consequences of an economic crisis is the sharp rise in fraud.

Understanding the correlation between financial hardship and deceptive practices is essential for businesses, regulatory bodies, and individuals. In a recessionary environment, the pressure to maintain appearances, survive financially, or exploit systemic vulnerabilities becomes a catalyst for illicit activities.

The Fraud Triangle: Why Crises Breed Deception

To understand why fraud spikes during an economic crisis, criminologists and auditors often point to the Fraud Triangle. Developed by Donald Cressey, this model explains the three factors that must be present for an individual to commit fraud: Pressure, Opportunity, and Rationalization.

1. Increased Financial Pressure

During a crisis, pressure is the primary driver. For individuals, this might be the sudden loss of a job, mounting debt, or the inability to provide for a family. For corporate executives, the pressure often manifests as the need to meet unrealistic earnings targets to prevent stock prices from plummeting or to secure much-needed credit lines. When survival is at stake, the boundary between ethical behavior and “doing what is necessary” begins to blur.

2. Expanded Opportunity

Economic downturns often lead to corporate downsizing. To cut costs, companies frequently reduce their headcount in administrative and oversight roles. When internal controls are weakened and duties are no longer segregated, opportunities for embezzlement and procurement fraud skyrocket. Furthermore, governments often rush to distribute stimulus funds or emergency loans with minimal vetting to provide immediate relief, creating a massive vacuum for bad actors to exploit.

3. New Forms of Rationalization

In a crisis, fraudsters often convince themselves that their actions are justified. An employee might steal from a company because they haven’t received a raise in years, or a business owner might underreport taxes to “save the jobs” of their employees. The narrative shifts from “I am committing a crime” to “I am a victim of the economy, and I am just evening the scales.”

Common Types of Fraud During a Recession

The methods used by fraudsters evolve to match the specific anxieties of the time. During an economic crisis, several specific types of fraud typically see a measurable uptick:

Corporate and Financial Statement Fraud

When markets are bullish, growth covers many sins. However, when the tide goes out, “creative accounting” becomes a tool for survival. Companies may inflate assets, hide liabilities, or record revenue prematurely to maintain investor confidence. The collapse of major firms often occurs during these periods as the gap between reported success and actual liquidity becomes impossible to bridge.

Investment Scams and Ponzi Schemes

Desperation for high returns in a low-yield or crashing market makes individuals vulnerable to “get-rich-quick” schemes. Fraudsters capitalize on the fear of missing out (FOMO) or the desire to recoup lost savings. History’s most famous Ponzi schemes are often unraveled during crises because the flow of new capital stops, but new ones are simultaneously born from the ashes of the old.

Cyber-Enabled Financial Crime

As more transactions move online during global disruptions, the digital surface area for fraud increases. Phishing attacks, ransomware, and identity theft become more sophisticated. Fraudsters often mimic government agencies or financial institutions, offering “debt relief” or “emergency grants” to harvest sensitive personal information.

Occupational Fraud

This is fraud committed by employees against their employers. It can range from simple expense account padding to complex vendor kickback schemes. In a crisis, the perceived “unfairness” of executive bonuses while lower-level staff face layoffs can trigger a surge in internal theft.

The Role of Technology and Digital Vulnerabilities

Modern economic crises are unique because of our total reliance on digital infrastructure. The speed at which information—and misinformation—travels can exacerbate fraud risks.

- Deepfakes and Social Engineering: Advanced AI can now mimic the voices or faces of CEOs to authorize fraudulent wire transfers (Business Email Compromise).

- Cryptocurrency Volatility: The lack of regulation in some digital asset spaces makes them a breeding ground for “rug pulls” and fake investment platforms during times of fiat currency instability.

Mitigation Strategies: Strengthening the Shield

While the risk of fraud increases during a crisis, it is not an inevitable fate. Organizations and individuals can take proactive steps to safeguard their assets.

For Organizations:

- Maintain Internal Controls: Even during layoffs, do not compromise on the segregation of duties. Ensure that the person who authorizes a payment is not the same person who reconciles the books.

- Continuous Monitoring: Use data analytics to spot anomalies in real-time. Modern software can flag unusual transaction patterns that might indicate kickbacks or ghost employees.

- Promote a Culture of Ethics: A “tone at the top” that prioritizes integrity over “growth at any cost” is the strongest deterrent to fraud.

- Whistleblower Protection: Most frauds are caught via tips. Ensuring employees have a safe, anonymous way to report suspicious activity is vital.

For Individuals:

- Verify Before You Trust: Never provide personal information or “processing fees” for unsolicited offers of financial aid.

- Monitor Financial Accounts: Regularly check bank statements and credit reports for unauthorized activity.

- Diversify Awareness: Stay informed about the latest scam tactics. Education is the first line of defense against social engineering.

Conclusion

Economic crises do more than just shrink GDP; they test the moral fabric of society and the resilience of our financial systems. By understanding that fraud is a predictable byproduct of economic stress, we can better prepare for it. Resilience is not just about surviving the financial loss—it’s about maintaining the integrity and trust that allow a market to eventually recover.

In a world where volatility is the new normal, vigilance remains the most valuable currency. Whether through robust corporate governance or individual skepticism, the fight against fraud is a continuous effort that becomes most critical when the economy is at its weakest.

Key Takeaways for Financial Safety

- Awareness: Recognize that fraud risks increase proportionally with economic uncertainty.

- Control: Do not let cost-cutting measures weaken your organization’s oversight.

- Verification: Always validate the source of financial opportunities, especially those that seem “too good to be true.”