Financial security is a cornerstone of modern life, yet the allure of “get-rich-quick” schemes remains a persistent threat to investors worldwide. Among the most notorious of these deceptions is the Ponzi scheme. Named after Charles Ponzi, who became infamous for his fraudulent activities in the 1920s, this type of investment fraud continues to evolve in the digital age.

Understanding the mechanics, history, and warning signs of Ponzi schemes is essential for anyone looking to navigate the complex world of finance safely.

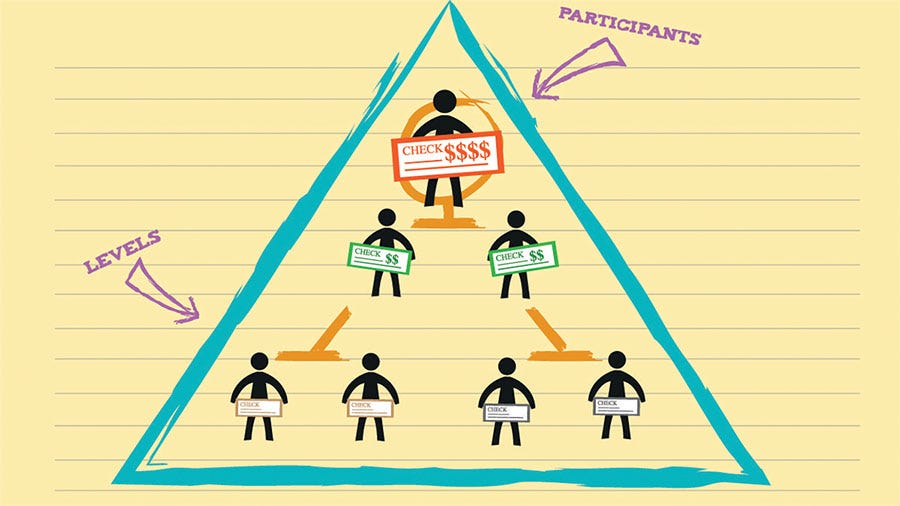

What is a Ponzi Scheme?

A Ponzi scheme is a sophisticated form of investment fraud that pays returns to earlier investors using the capital provided by newer investors. At its core, the scheme is a “robbing Peter to pay Paul” scenario. Unlike a legitimate investment, where profits are generated through business activities, trade, or asset appreciation, a Ponzi scheme has no underlying source of wealth.

How the Cycle Works:

- The Hook: A promoter promises high returns with little to no risk.

- The Early Success: The first few investors receive the promised high returns, which builds credibility.

- The Recruitment: Encouraged by their “profits,” early investors tell others or reinvest their own money.

- The Collapse: The scheme requires a constant, growing stream of new money to pay previous participants. When recruitment slows down or a large number of investors try to withdraw their funds simultaneously, the house of cards collapses.

The Namesake: Charles Ponzi and the Postage Stamp Scandal

While Charles Ponzi did not invent this method of fraud, his scale and audacity in 1920 earned him a place in history. Ponzi discovered a loophole involving International Reply Coupons (IRCs). These coupons could be bought in one country and exchanged for postage stamps in another. Because of fluctuating exchange rates, Ponzi claimed he could buy IRCs cheaply in Europe and redeem them for higher values in the United States.

He promised investors a 50% return in 45 days or a 100% return in 90 days. In reality, the logistics of moving and exchanging millions of coupons were impossible. Ponzi simply used money from new investors to pay off the old ones. By the time the scheme was exposed by the Boston Post, Ponzi had raked in an estimated $20 million (equivalent to nearly $300 million today), leaving thousands of families devastated.

The Largest Fraud in History: Bernie Madoff

The most significant evolution of the Ponzi scheme occurred decades later with Bernie Madoff. Unlike Ponzi, who targeted the general public, Madoff was a respected figure on Wall Street and a former chairman of the NASDAQ.

For over 20 years, Madoff ran an investment firm that appeared to produce consistent, moderate returns regardless of market conditions. This “consistency” was his greatest weapon, as it didn’t raise the immediate red flags that astronomical returns usually do. However, in 2008, during the global financial crisis, the influx of new capital dried up, and investors began demanding their money back.

Madoff eventually confessed to his sons that his multi-billion dollar investment business was “one big lie.” The fraud was valued at approximately $64.8 billion, affecting charities, celebrities, and individual retirees globally.

Red Flags: How to Spot a Ponzi Scheme

Modern fraudsters use sophisticated technology, including cryptocurrency and Forex trading bots, to mask the old Ponzi structure. Regardless of the “product” being sold, certain red flags remain constant:

- High Returns with Little or No Risk: All investments carry some degree of risk. Any guarantee of high returns is a major warning sign.

- Overly Consistent Returns: Markets fluctuate. If an investment produces steady positive returns even when the economy is struggling, it may be fabricated.

- Unregistered Investments: Most legitimate investment opportunities are registered with national regulators (like the SEC in the U.S. or BaFin in Germany).

- Secretive or Complex Strategies: If you cannot understand how the money is being made, or if the promoter claims the strategy is “proprietary” or “too complex to explain,” proceed with extreme caution.

- Difficulty Receiving Payments: If you face hurdles when trying to withdraw your money or are pressured to “roll over” your returns for even higher payouts, the scheme may be running out of cash.

The Role of Cybersecurity in Modern Fraud

In the 21st century, Ponzi schemes have migrated online. Fraudsters use social media, “finfluencers,” and encrypted messaging apps to reach a global audience. Phishing and identity theft are often used to gain the trust of potential victims or to drain assets once a user joins a platform.

Protecting oneself involves more than just financial literacy; it requires digital hygiene. Always use two-factor authentication (2FA) on financial accounts and verify the credentials of any “advisor” through official regulatory databases.

Lessons for the Modern Investor

The history of Ponzi schemes offers several timeless lessons:

- Due Diligence is Mandatory: Never invest money based on a “tip” or social media hype. Verify the legitimacy of the firm and the individual offering the investment.

- Diversification is Protection: Ponzi schemes often encourage victims to “go all in.” By spreading your investments across different asset classes (ETFs, stocks, bonds), you limit your exposure to any single fraudulent entity.

- If it Sounds Too Good to be True, It Is: Human psychology is wired to seek shortcuts to wealth. Recognizing this bias is the first step in defending against fraud.

- The Importance of Regulation: Support and use financial institutions that are transparent and subject to oversight. Regulation provides the audits and “paper trails” that Ponzi schemes try to avoid.

Conclusion

The Ponzi scheme is a chameleon, changing its colors to match the latest economic trends—from postage stamps and real estate to Bitcoin and AI. However, the underlying mechanics remain the same: a reliance on deception and the constant recruitment of new capital.

By staying informed, practicing skepticism, and prioritizing security, investors can protect their hard-earned capital from the “financial predators” of the digital age. History shows us that while the names of the fraudsters change, the lessons remain the same: true wealth is built through patience, transparency, and sound economic principles.

Would you like me to translate this article into German or Portuguese, or perhaps create a social media summary for it?