In the interconnected landscape of 2026, the global financial system operates at a speed once unimaginable. Digital transactions are near-instantaneous, and artificial intelligence (AI) manages everything from high-frequency trading to personal wealth. However, this evolution has brought a shadow: financial fraud. No longer confined to simple “phishing” emails, modern financial crime is a sophisticated, multi-billion-dollar industry that threatens the very stability of global markets.

Understanding the impact of financial fraud is no longer just a concern for compliance officers; it is a critical macroeconomic issue. As of 2026, the costs are not merely financial—they are systemic, eroding trust and distorting market efficiency.

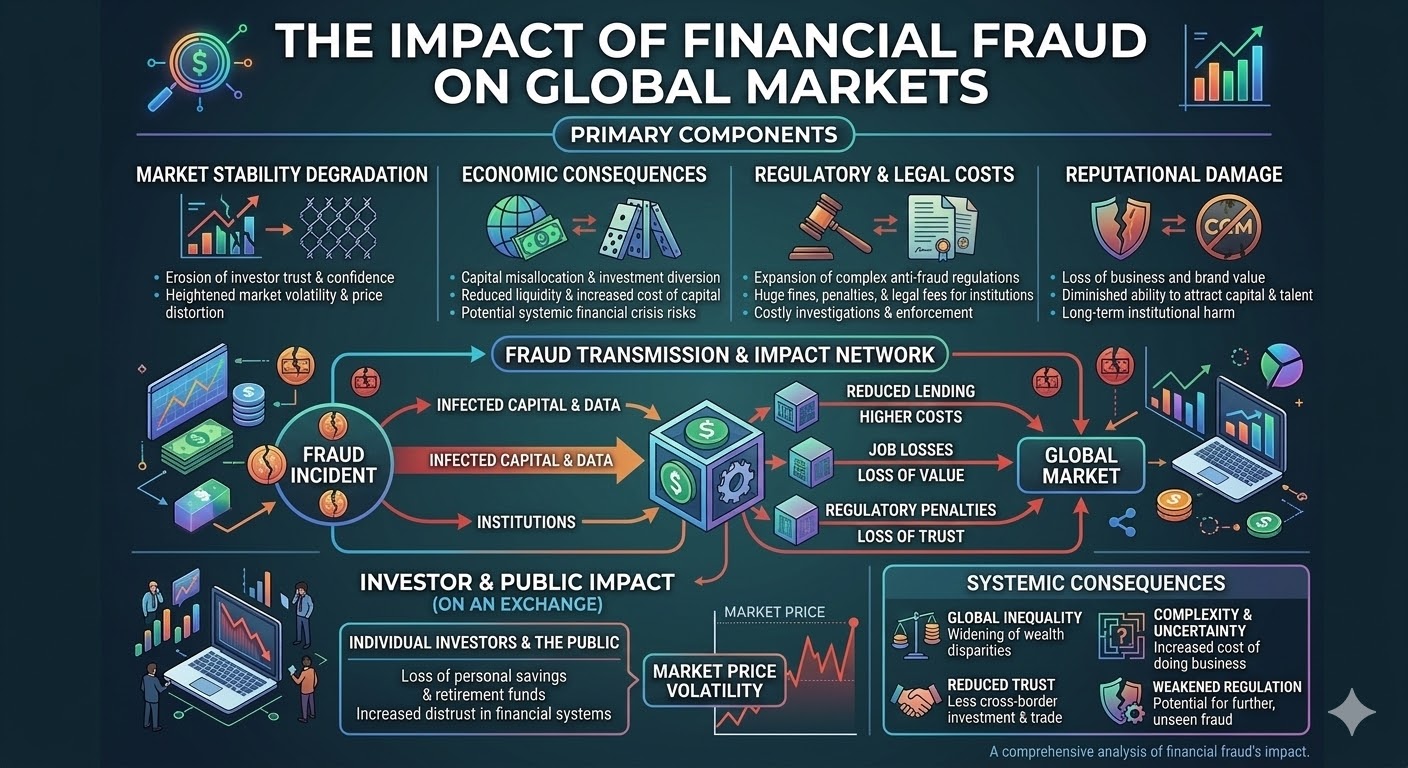

The Massive Scale of the Fraud Crisis

Recent data from early 2026 indicates that global fraud losses in financial services have continued their steep upward trajectory. Estimates suggest that total global losses related to scams and fraudulent activities reached approximately $450 billion in the past year alone.

This surge is driven by several key factors:

- AI-Generated Identities: Criminals now use generative AI to create “synthetic identities”—fictional personas with real credit histories—making them nearly impossible to distinguish from legitimate customers.

- Deepfakes in Biometrics: With deepfake technology now accounting for nearly 40% of biometric fraud cases, traditional security measures like “video selfies” for bank onboarding are being compromised.

- Real-Time Payment Exploitation: The shift toward always-on, instant payment systems allows fraudsters to move stolen funds across borders before traditional fraud detection systems can flag the transaction.

Direct and Indirect Economic Consequences

The impact of financial fraud radiates through the global economy in layers, from individual victims to national GDPs.

1. Direct Financial Losses and Market Volatility

The most immediate effect is the drainage of capital. When a major financial institution is hit by a large-scale cyber-fraud event, the market reaction is often swift. In “high-trust” markets like the US and EU, a single major accounting scandal or fraud revelation can lead to a significant drop in stock prices—not just for the affected firm, but for the entire sector. This “contagion effect” creates unnecessary volatility and scares off retail investors.

2. Erosion of Public Trust

Trust is the “invisible currency” of the financial world. When fraud becomes rampant, the public begins to withdraw. According to the Gasa Global State of Scams 2025/2026 Report, nearly 70% of adults worldwide encountered a scam in the last 12 months. This widespread exposure leads to “scam fatigue,” where consumers become hesitant to adopt new financial technologies (FinTech), slowing down the pace of global economic innovation.

3. Operational Costs for Institutions

Financial institutions are no longer just banks; they are security firms. In 2026, companies are losing an average of 5% of their annual revenue to fraud. To combat this, banks are pouring billions into “FRAML” (the convergence of Fraud and Anti-Money Laundering) platforms. While necessary, these massive expenditures on compliance and defense are resources diverted away from productive lending and investment.

The AI Paradox: Weapon and Shield

AI is the defining feature of financial fraud in 2026. It serves as both the primary tool for criminals and the most effective defense for institutions.

The Malicious Use of AI:

Fraudsters now utilize “Agentic AI”—autonomous bots that can carry out complex social engineering attacks. These bots can engage in weeks-long conversations with targets, mimicking the tone of a trusted advisor or family member, leading to “Authorized Push Payment” (APP) fraud where the victim willingly, but mistakenly, sends money to a criminal.

The AI Defense:

Conversely, 85% of financial institutions reported seeing positive returns from using AI for real-time detection in early 2026. Modern AI systems can analyze millions of data points—such as typing speed, mouse movements, and IP consistency—to identify a fraudulent actor in milliseconds.

Key Trend: By late 2026, the EU’s Digital ID Wallet and India’s Aadhaar system are becoming the gold standards for “Digital Identity,” providing a cryptographic layer of protection that moves beyond vulnerable passwords and SMS codes.

Impact on Emerging Economies

While developed nations have the infrastructure to absorb some shocks, the impact of financial fraud on emerging markets is often devastating.

- Capital Flight: High levels of fraud can lead international investors to view a country as “high risk,” causing capital flight and currency devaluation.

- Stifled Growth: In regions like Sub-Saharan Africa, illicit financial flows drain domestic revenues that are desperately needed for infrastructure and education.

- Social Fragmentation: Fraud often targets the most vulnerable, exacerbating wealth inequality and leading to social unrest when life savings are lost without hope of reimbursement.

Regulatory Responses and the Way Forward

In response to these threats, 2026 has seen a landmark shift in global regulation. We are moving from “static” compliance to “outcome-based” effectiveness.

| Initiative | Goal | Impact |

| EU Digital ID Wallet | Universal biometric authentication | Reduces identity theft by 90% in pilot phases. |

| UK Reimbursement Scheme | Mandatory bank refunds for victims | Increases bank accountability for security flaws. |

| Cross-Border Intelligence | Real-time data sharing between nations | Breaks down silos that fraudsters use to hide. |

The future of global market stability depends on collaboration. Fraudsters operate without borders; therefore, regulators and financial institutions must share intelligence with the same speed and fluidity as the criminals they are chasing.

Conclusion

The impact of financial fraud on global markets in 2026 is a complex, evolving challenge. While it poses a significant threat to market integrity and consumer trust, it is also driving a revolution in security technology. The “arms race” between AI-powered criminals and AI-powered defenders will define the financial landscape for the next decade.

To maintain a healthy global economy, the focus must remain on building resilience, not just resistance. By integrating digital identity, real-time AI monitoring, and international cooperation, the global market can protect its most valuable asset: the trust of its participants.

Would you like me to generate a summary of the most common types of financial fraud seen in 2026 to accompany this article?